THE NEW W-4 IS COMING: HERE’S WHAT YOU NEED TO KNOW

The IRS has introduced a new Form W-4 for 2020 that will go into use on January 1, 2020. Why is the IRS revising the W-4? In short, accuracy. The new form is designed to help withholding amounts match up more closely with what an employee’s tax burden will be for the year.

No doubt employers and employees will have many questions. Here’s what they need to know.

What is changing?

- The biggest change: there are no more allowances.

- Employees will no longer be able to request adjustments to their withholding based on allowances.

- Instead the new form has a 5-step process that gives employees the opportunity to record income earned from second job as well as spouse’s income.

- An individual’s tax obligation for the year is based on combined income from all sources. Employees who have other income sources and are concerned they will owe additional taxes at the time of filing may want to complete Step 4.

- Keep reading for more in-depth instructions about how to fill out the new form.

Do all employees need to fill out the new form?

- The answer is no. Employees who have submitted a Form W-4 in any year before 2020 will not be required to submit a new form.

Who does need to fill out the new form?

- All employees hired after January 1, 2020 are required to use the new form.

- Any employee who wants to change his or her withholding amount needs to complete the new form.

Review our step-by-step guide for completing the new W-4.

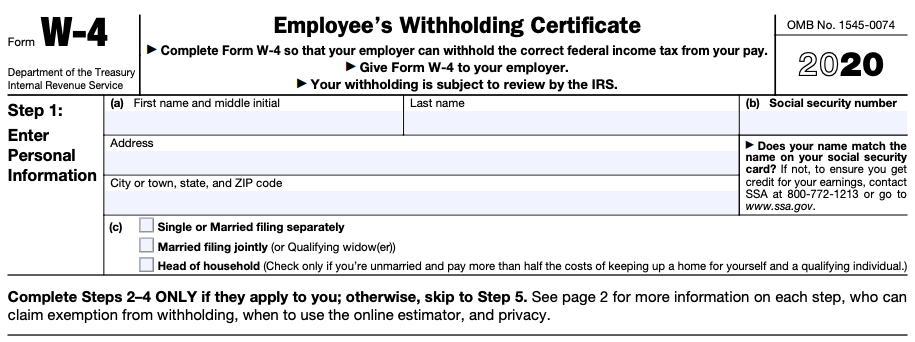

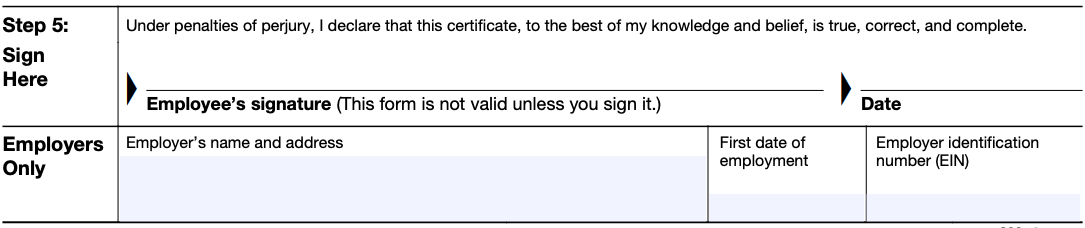

The new Form W-4 has 5 steps. Employees are only required to fill out Step 1 and Step 5, so let’s start with those.

Step 1 includes name, address and filing status.

Step 5 at the bottom of the page is where the employee signs the form.

Step 1 and Step 5 are the only sections that must be filled out. Many employees will complete only these 2 steps, and their tax withholding will be calculated based on their filing status and tax rate for their income.

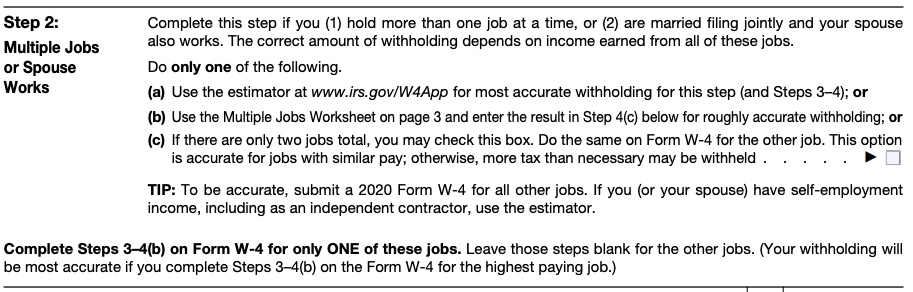

Now let’s take a look at Steps 2, 3 and 4, which employees will complete only if these steps apply to their situation.

Step 2 provides an employee with options for listing their spouse’s income or income earned from a second job.

As described in Step 2(a), an employee can visit the Tax Withholding Estimator to get the best estimation of what their tax obligation will be for the year and determine if they should withhold an additional amount in Step 4(c). This might be a good idea for employees who have multiple jobs in a year or a complex income situation. But this can get complicated and confusing, and employees do not have to do this step at all.

Some employees do not want to disclose to their employer that they have a second job. If this is the case, they should not check the (c) box. Instead they can follow the options explained in (a) or (b) or skip this step altogether.

Step 3 is where an employee claims dependents. The section is pretty straightforward. An employee will multiply the number of qualifying children by $2,000. An employee can also include dependents other than children. What is a qualifying child? Read the IRS Qualifying Child Rules.

Step 4 is where employee can made additional adjustments.

Employees who want to record income from other sources (though not from another job) can do so in Step 4 (a).

Employees who know they will claim other deductions on their federal taxes (medical expenses, mortgage interest deduction, for example) can record that information in Step 4 (b). Note that this is any deduction that they want to claim on top of the standard deduction, which is $12,400 for an individual.

Finally, employees who have calculated their estimated tax burden using the IRS Tax Withholding Estimator calculator and have determined they want an additional amount withheld can list that in Step 4(c).

Once again, employees are not required to fill out Step 4. If an employee is confused about what they should put in this section or whether it applies, he or she does not have to complete this part of the form.

How does this affect employees who claim exemption from withholding?

- Most people do not meet the criteria to be exempt from withholding. However, an employee who does meet the criteria may claim exemption from withholding by writing “Exempt” in Step 4(c). They must complete the new Form W-4 for 2020 to have no income tax withheld from their paycheck.

- They will also need to complete a new Form W-4 by February 15 of every year to continue to claim exemption from withholding.

- By law, employers are required to use the information an employee provides on his or her signed W-4 when withholding from employee pay.

Anthros will provide all clients with an updated New Hire Packet containing the new W-4 to use beginning on January 1.

The Anthros team is available to help clients understand the new Form W-4. If you have questions about the new form and what effect it will have on your organization, please contact us.

About the Author

Helen Usher is the Director of Benefits at Anthros Inc.

{kind=link}